One question we’re often asked by advisers, is “when is the right time to quote my fee?”. It’s one thing to determine how much to charge, it’s also incredibly important to know how and when to position it with your clients. The following is an excerpt from the revised edition of my book, Pricing advice:

Selling your services as a financial adviser and, more importantly, actually providing advice to clients is all about communication. The problem is that when it comes to

financial advice, people have a lot to absorb when they meet with their planner, so there is an art to the timing of your communication.

This is especially so when they are learning new things, and dealing with something as emotional as their money and its impact on their hopes and dreams. You could tell two people exactly the same thing and they would process it differently, based on how you tell them, their pre-existing knowledge of the subject, what else is on their mind at the time, and many other factors.

The timing of when to detail your fee to a new client is important—too early and they’ll decide on cost not value; too late and you’ll run the risk of doing an awful lot of work without getting paid.

In the context of engaging a new client, you will probably have much greater success if you discuss your fees in detail after spending your first meeting getting to know

them and giving them an idea of your personality and professionalism. Avoid telling them what your fees are, prior to telling them what your fees do.

Be clear that your engagement fee provides access to your intellectual property and your advice on how to structure and manage their finances in order to allow them to achieve their objectives.

Your ongoing fee gives them your support and accountability to ensure that they keep doing the right things regardless of what life throws at them, or what happens with

legislative reform and economic fluctuations.

Detailing your engagement fee after your first meeting allows the client to gain some sense of the value of your fee. Detailing your ongoing fees and corresponding service

package after you have spent time together to create and understand their financial plan will allow them to make an informed decision on whether they require ongoing

services.

If you commence work for the client and create their financial plan before reaching agreement on your engagement fee, you are missing your opportunity to obtain

their approval at their critical moment of need. You are also opening yourself up to disputes at a later time.

Let’s focus a little more now on your new client process, to ensure that you can communicate your advice and value well.

When you receive an enquiry from someone that fits the description of your preferred clientele, you want to put them in a position to see value in your services and engage you, so how can you maximise the probability of that happening?

The process that you take clients through is just as important as the conversations you have, or the documents you use to promote your advice. Many advisers are accustomed to conducting one meeting with a client and then placing an SOA in front of them in the second, expecting a signature on the Authority To Proceed. Whilst they often get a signature, and successfully make a sale, they may not have built a firm enough foundation for a strong ongoing relationship yet.

Moreover, if they have provided a comprehensive plan, they are unlikely to have spent enough time educating the client about the strategies employed, or investment markets, risk and return, etc.

We would argue that to create a long-term relationship with your clients, you need to spend enough time to get to know them well, and to allow them to understand their financial plan, and embrace it.

Clients will now be fully aware of how much they are paying you to provide advice, and you will have far greater success if you take them on a journey to understand their financial plan, and if they are involved in its creation.

For a client to happily engage your ongoing service package and not suffer buyers remorse, you will have to spend more than just two meetings to truly engage them.

If you are creating a comprehensive financial plan, there is almost certainly too much information for them to absorb in one meeting. You need to help them understand enough about your recommendations and enough about your services and expertise that they will not only embrace their financial plan but also be happy to pay your ongoing fees and engage you for the next decade or three.

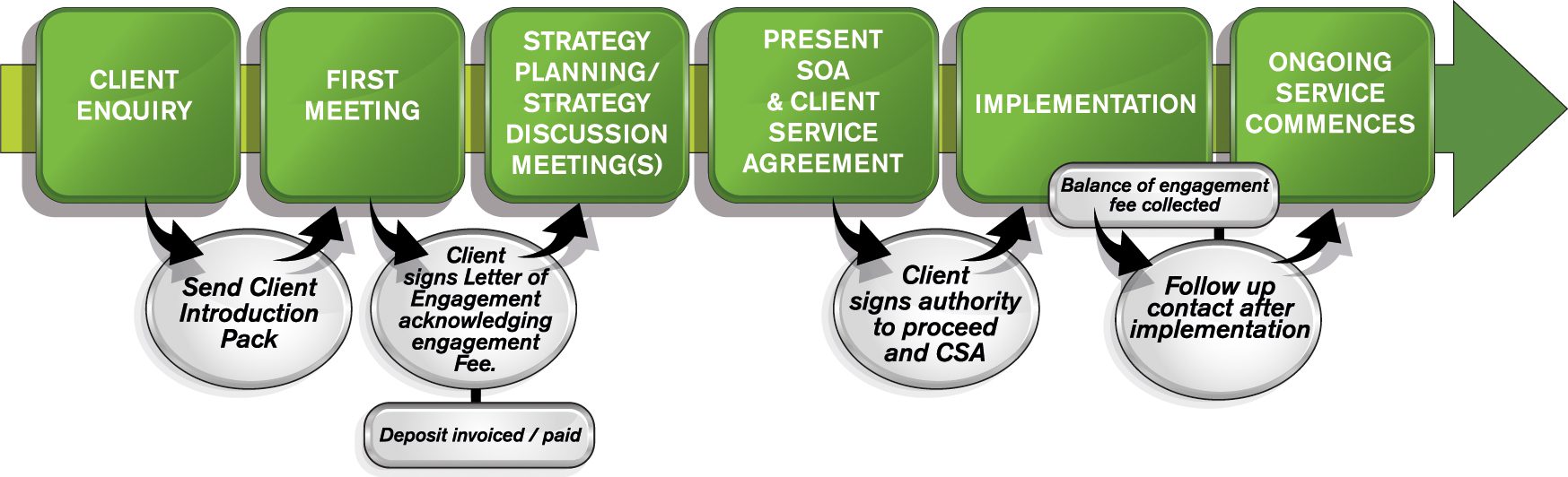

Your new client process should look something like this: We break down each of these steps in further detail in the book, which can be obtained from our website in both hard copy and as an eBook.

We break down each of these steps in further detail in the book, which can be obtained from our website in both hard copy and as an eBook.

Note that the flowchart pictured is designed for adviser/office use only. It can also be helpful, to enable your client to understand what is involved in your engagement process and what their responsibilities will be (in addition to paying your fee), to use a client-friendly diagram to demonstrate what will happen from the time they enquire with you, to when your advice is provided and implemented. There is a template available for you to customise on our website.